By Hernan Lopez.

Companies mentioned: Alphabet, Amazon, ByteDance, CBS, Collective Artists Network, Deezer, Disney, Fox, Google, iQIYI, LionTree, Meta, Netflix, NBCUniversal, Paramount Skydance, Roku, Samba TV, TikTok, UFC, YouTube.

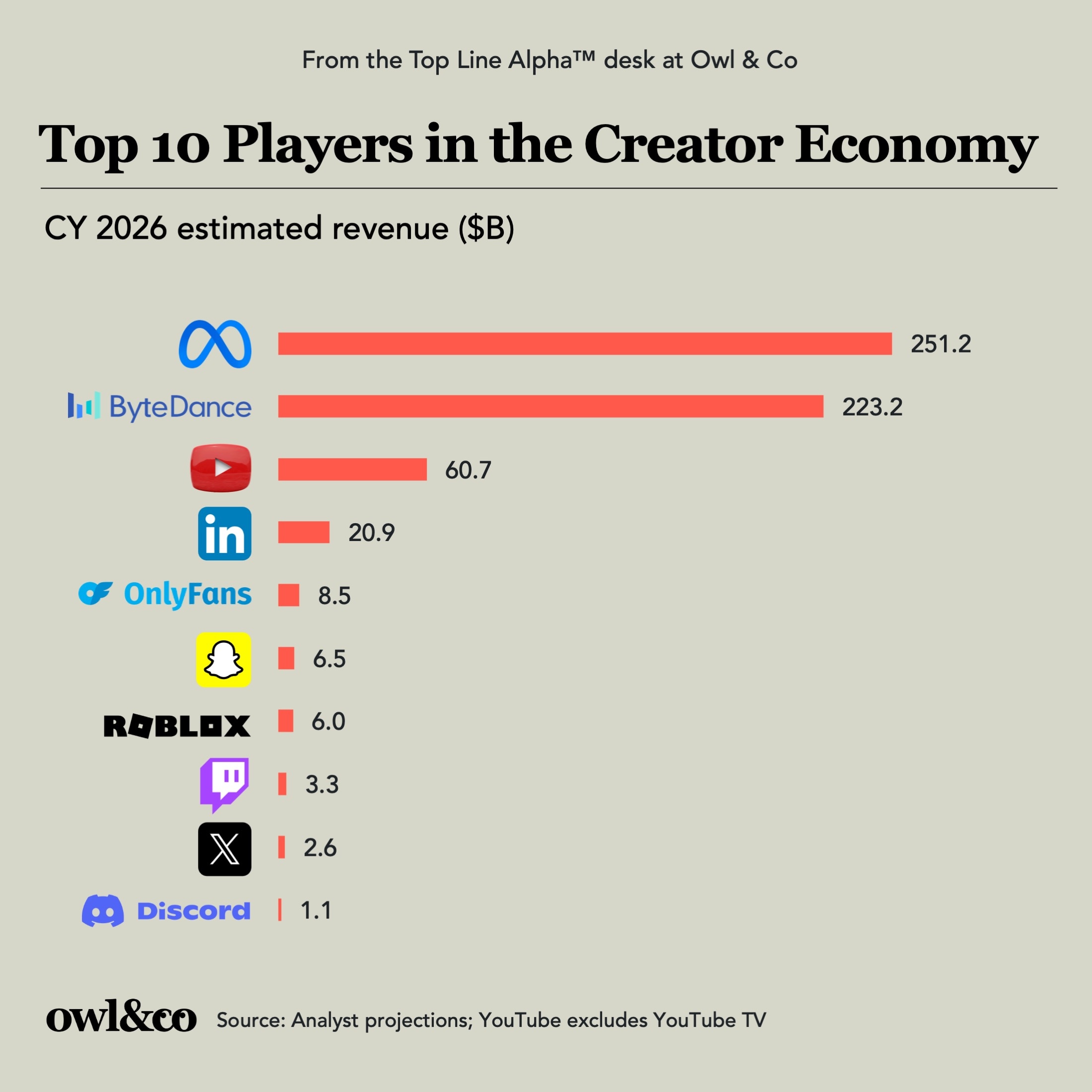

Questions answered: How do Netflix's four overlapping S-curves stack up, and what's the fifth? Whose TAM is bigger: Netflix's or the creator economy's? How much does the average Netflix advertiser spend a year, and what does that tell us about how to grow streaming advertising?

Special note: This is a public version of the Streamonomics® newsletter. I send an exclusive version to Owl & Co clients one day in advance, which includes more in-depth analysis, access to Owl & Co proprietary research, and additional charts. If you work for an Owl & Co client (or would like to become one), just hit reply.

“We’ve captured about 7% of addressable revenue; this is in countries and categories that we currently directly participate in. We now estimate that number at $670B in 2026, and that grows, year-on-year.” That was Greg Peters at the top of Netflix’s most recent earnings call, aware that Netflix’s EV had dropped from $460B to $420B shortly after reporting solid Q1 results. Netflix had reaffirmed, not raised, full-year guidance.

Large-cap companies rarely talk about their Total Addressable Market (TAM) outside of investor day presentations...