By Hernan Lopez.

Companies mentioned: Amazon, Disney, Netflix, Paramount, Peacock, Spotify, WBD, YouTube.

Questions answered: What likely accounts for ~65% of Paramount’s $6B in synergies? What two side effects exist of AI not being used properly? What does it take to be the executive, creator, or investor who comes out of this reorganization stronger?

Special note: This is a public version of the Streamonomics® newsletter. I send an exclusive version to Owl & Co clients one day in advance, which includes more in-depth analysis, access to Owl & Co proprietary research, and additional charts. If you work for an Owl & Co client (or would like to become one), just hit reply.

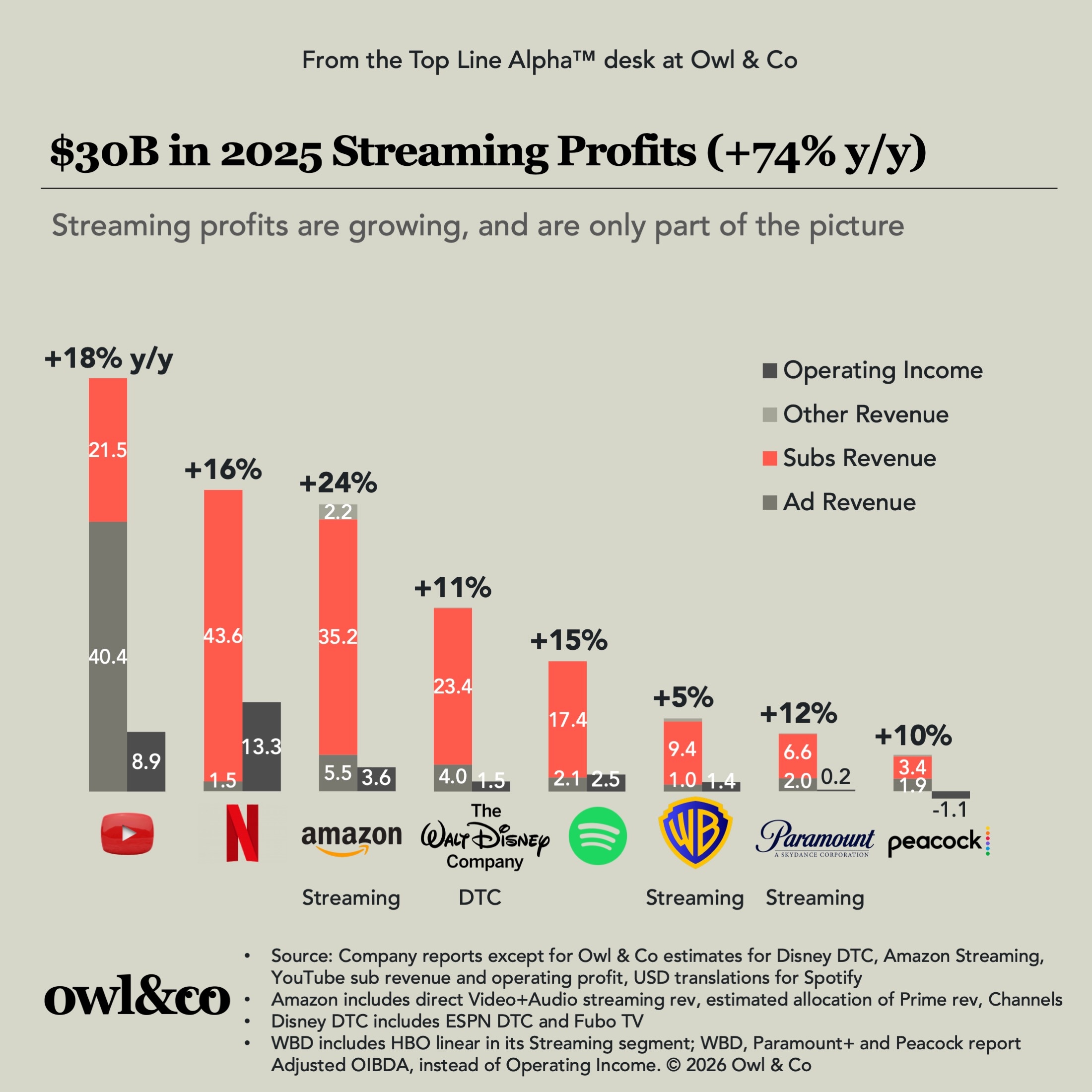

Last week I posted a chart that opened lots of eyes (and not just because of the fine print). YouTube, Netflix, Amazon, Disney, Spotify, Paramount, WBD and Peacock collectively made $30B in profits from streaming in 2025, up 74% from the year before. And only 44% of that figure came from Netflix. There was a sentiment a couple of years ago that “the streaming wars are over.” I always understood the feeling: Netflix was so far ahead of any other streamers following its business model that there was no comparison.